What Does RBI Authorisation Mean for a Remittance Platform?

India heavily regulates money transfers through its payments system, and every legitimate remittance platform must comply with specific rules set by the Reserve Bank of India. This blog explains what RBI authorisation means for a remittance app, outlines the three main licensing routes available (RDA, MTSS, and the newer PA-CB framework), and shows what this authorisation signals to senders. It also explains how to verify whether a platform is genuinely RBI-authorised and highlights the warning signs that suggest a platform may operate outside the regulatory framework. Finally, the blog explores how we structure our operations within India’s compliance system while still keeping fees low and exchange rates transparent.

Reserve Bank of India grants authorisation to remittance platforms that facilitate cross-border money transfers into or out of the country. The RBI issues this authorisation under specific frameworks such as the Money Transfer Service Scheme (MTSS), the Rupee Drawing Arrangement (RDA), or the newer Payment Aggregator Cross Border (PA-CB) licence introduced in October 2023.

In simple terms, a platform cannot legally move foreign currency into an Indian bank account unless it holds one of these authorisations or partners with an authorised entity. The Foreign Exchange Management Act of 1999 and the Payment and Settlement Systems Act of 2007 give the RBI the authority to regulate India’s cross-border payments ecosystem and decide which entities can operate within it.

This authorisation matters because the channel handling your transfer determines the legal validity and security of the transaction. Authorised channels maintain proper records, follow KYC requirements, and protect both the sender and the recipient. Unauthorised channels bypass these safeguards.

Why RBI regulate international remittances so tightly

India is the world’s largest recipient of remittances. The World Bank pegged inflows at $129.1 billion in 2024, which makes the country’s inward remittance corridor a serious financial artery. RBI’s job is to keep that artery clean.

There are five practical reasons RBI insists on authorisation:

FEMA compliance.

Every rupee crossing the border has to follow the Foreign Exchange Management Act, including the right purpose code.

Anti-money laundering checks.

Authorised entities are required to run KYC, screen against sanction lists, and report suspicious activity to FIU-IND.

Balance of payments tracking.

RBI uses remittance data to manage the country’s foreign reserves and policy.

Consumer protection.

Senders and beneficiaries get a paper trail and a recourse path if something goes wrong.

Counter-terror financing controls.

Authorised platforms have to demonstrate they are not channels for illegal flows.

Skip the framework, and the same transfer that took thirty seconds on an app becomes a FEMA violation that can attract a penalty of up to three times the transaction amount.

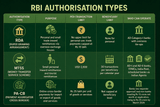

The three main RBI authorisation paths for a remittance platform

Most fintechs that move money into India operate under one of three frameworks. Each has its own limits, target use case, and eligibility criteria. The table below lays them out side by side.

Rupee Drawing Arrangement (RDA)

RDA serves as the primary framework for personal inward remittances in India. It operates through partnerships between RBI-approved AD Category-I banks in India and licensed exchange houses in the sender’s country. When you send money to India through an app that settles transfers through an RDA partnership, a regulated Indian bank handles the rupee settlement instead of the app itself.

RDA allows unlimited personal remittance amounts, which makes it the preferred route for larger family transfers, education payments, and similar transactions. However, the framework caps trade-related transactions at ₹15 lakh per transfer to keep the system focused on personal remittance flows.

Money Transfer Service Scheme (MTSS)

MTSS is designed for fast, small-value personal remittances. Think Western Union or MoneyGram at the high street level. The cap of USD 2,500 per transaction and 30 transactions per beneficiary per year keeps it firmly in the small remittance bracket.

Cash payouts up to Rs 50,000 are allowed for resident beneficiaries, with anything above that having to go to a bank account. MTSS is strictly for personal use. Sending money to an NRE or NRO account, or paying for goods, is not permitted under this scheme.

Payment Aggregator Cross Border (PA-CB)

PA-CB is the newest and most ambitious framework. RBI introduced it on October 31, 2023, to bring all online cross-border payment facilitators (previously known as OPGSPs) under direct regulation. It splits authorisation into three categories: PA-Export, PA-Import, and PA-Export-and-Import.

Non-bank entities seeking PA-CB authorisation need a minimum net worth of Rs 15 crore at the time of application, rising to Rs 25 crore by March 31, 2026. They also have to register with the Financial Intelligence Unit of India before applying. AD Category-I banks can perform PA-CB activity without separate RBI approval.

For background on how cross-border payment rails have evolved, this piece on how stablecoin rails make remittances faster and cheaper covers the technology side of the same shift RBI is now regulating.

What RBI authorisation actually means for you as a sender

When you send money through an RBI-authorised platform, five things happen quietly in the background that you would otherwise not get.

First, your funds travel through a tracked and audited channel. There is a paper trail.

Second, your KYC is performed to Indian standards, which means your transfer will not get flagged or frozen on arrival.

Third, every transfer carries a FEMA purpose code, which matters when the beneficiary’s bank or the tax authorities ask why the money came in.

Fourth, you get a real recourse path if something goes wrong, through the banking ombudsman or directly to the RBI.

Fifth, the transfer generates the right documentation for tax reporting, including the FIRC (Foreign Inward Remittance Certificate), where applicable.

None of this is glamorous. But the absence of any of it is exactly what makes informal channels risky, no matter how good the rate looks.

There is a useful overview of compliant transfer steps for sending money safely to India that walks through what an authorised flow looks like in practice.

How to check if a remittance platform is RBI-authorised

A few quick checks tell you almost everything:

- Look up the platform, or its banking partner, on RBI’s published list of entities authorised under the Payment and Settlement Systems Act 2007 (available on rbi.org.in).

- Read the platform’s regulatory disclosure page. A serious operator will name its banking partner, its AD-I or AD-II affiliation, and its FIU-IND registration status.

- Check whether the platform names a specific scheduled commercial bank as its rupee-side partner. Vague language like “we work with leading banks” without naming one is a warning sign.

- Verify the rupee credit on the receiving side comes via NEFT, RTGS, or IMPS from a recognised Indian bank, with a clear purpose code.

- For platforms handling larger amounts or specific corridors, check that they reference the right framework (RDA for large personal, MTSS for small personal, PA-CB for trade or e-commerce).

Red flags of an unauthorised remittance platform

If you spot any of the following, the platform is either operating in a grey zone or outside the system entirely:

- Promises of no documentation regardless of the amount sent.

- Requests to deposit funds into a personal bank account in the source country before the rupee transfer is initiated.

- No named Indian banking partner anywhere on the website or in the app.

- Exchange rates dramatically better than the live mid-market rate, with no clear explanation of how that is possible.

- No FEMA purpose code captured at the time of transfer.

- Use of informal hawala-style channels framed as “instant” or “cash-only” transfers.

- No FIU-IND registration mentioned in the platform’s disclosures.

The exchange rate trap is the most common one. Rates that look too good are usually subsidised by the platform during a launch phase (which is legitimate) or are simply impossible (which is a sign of an unregulated channel). For a deeper read on what actually drives rates, this explainer on the factors that affect the INR exchange rate is useful context.

How PandaMoney handles RBI compliance

PandaMoney combines fintech efficiency with India’s regulatory framework. The platform uses stablecoin rails such as USD Coin and Tether to move value across borders quickly and at lower costs. However, regulated banking partners operating under RBI-authorised frameworks always handle the final rupee settlement into the recipient’s Indian bank account.

In practical terms, this means every PandaMoney transfer carries a FEMA purpose code, undergoes KYC and source-of-funds checks where applicable, and lands via standard Indian banking rails (IMPS, NEFT, or RTGS) from an AD Category-I bank. Senders see a clean app with mid-market rates and zero transfer fees during the launch offer. The underlying compliance work happens in the background.

PandaMoney does not promise to bypass any RBI rule. It promises to make a fully compliant transfer feel as simple and cheap as it should have been all along. You can download the PandaMoney app on Android or iOS from getpanda. money to see the flow yourself. For senders worried about transfer limits and IRS reporting rules from the US side, the US-to-India guide pairs well with this one.

Frequently Asked Questions

Is RBI authorisation the same for inward and outward remittances?

No. Different sections of the FEMA framework govern inward remittances and outward remittances separately. Frameworks such as RDA, MTSS, and PA-CB typically regulate inward remittances, which involve money entering India. In contrast, the Liberalised Remittance Scheme (LRS) governs outward remittances and allows resident Indians to send up to USD 250,000 abroad per financial year for permitted purposes.

Does PandaMoney hold its own RBI licence, or does it partner with banks?

PandaMoney operates through regulated banking partners that hold the relevant RBI authorisations for the rupee leg of every transfer. This is a common and fully compliant model for fintechs, where the technology layer (PandaMoney’s app and stablecoin rails) sits on top of an authorised banking partner that handles the regulated rupee settlement. The end result is a single, smooth experience for the sender, with full FEMA compliance underneath.

What is the practical difference between RDA and MTSS for sending money to India?

RDA is the larger, more flexible channel. It has no upper limit for personal remittances and is the default route for substantial family transfers, education payments, and similar use cases. MTSS is the smaller, faster channel built around walk-in cash payouts and small remittances, with a USD 2,500 per-transaction cap and a 30-transactions-per-year limit per beneficiary. If you regularly send larger amounts home, your transfer almost certainly settles via RDA, not MTSS.

Can a fintech operate remittance services without any RBI authorisation?

Not legally. Any entity moving foreign currency into or out of India for customers’ needs requires either direct RBI authorisation or a clear, contracted partnership with an authorised entity (typically an AD Category-I bank or an authorised PA-CB). A platform that claims to operate “outside the banking system” for cross-border transfers is, by definition, operating outside FEMA. That exposes both the platform and its users to legal risk.

What happens if I send money through an unauthorised platform?

In the best case, the transfer simply gets delayed or rejected by the beneficiary’s bank. In the worst case, the funds get frozen pending investigation, and you (the sender) and the beneficiary can face FEMA penalties of up to three times the transaction amount. Beyond the legal risk, there is no banking ombudsman to complain to if things go wrong with an unauthorised channel. The platform can disappear, and you have very limited recourse.

Where can I verify a platform’s RBI authorisation status?

The Reserve Bank of India publishes lists of authorised entities under the Payment and Settlement Systems Act 2007 on rbi.org.in. You can also check the RBI’s list of authorised dealer banks, full-fledged money changers, and authorised PA-CBs. For most senders, the simplest check is to verify that the platform names a specific RBI-licensed banking partner, and that the rupee credit lands from that bank with a clear purpose code.

Disclaimer

This blog is for informational purposes only and does not constitute legal, financial, or tax advice. Regulations, fees, and exchange rates change frequently. Consult a qualified CA or tax advisor for guidance specific to your situation.

RBI and FEMA regulations are updated periodically. Always verify current guidelines at rbi.org.in. PandaMoney is a fintech platform, not a bank, and operates through regulated institution partners for the rupee leg of every transfer.

Exchange rates and transfer fees are indicative and subject to change. PandaMoney shows all costs transparently before you confirm any transfer.

GetPandaMoney Inc. is a financial technology company, not a bank. Our product and services are offered in partnership with regulated and licensed financial institutions in each jurisdiction that we operate in. Client(s) deal directly with our regulated partners through the platform provided by PandaMoney.

For any queries or grievances, please write to us at compliance@getpanda.money

131 Continental Dr Suite 305 Newark, DE, 19713 US

©2025 PandaMoney. All Rights Reserved.

GetPandaMoney Inc. is a financial technology company, not a bank. Our product and services are offered in partnership with regulated and licensed financial institutions in each jurisdiction that we operate in. Client(s) deal directly with our regulated partners through the platform provided by PandaMoney.

For any queries or grievances, please write to us at compliance@getpanda.money

131 Continental Dr Suite 305 Newark, DE, 19713 US

©2025 PandaMoney. All Rights Reserved.