USA vs UK vs Germany: India Remittance Fee Comparison

This guide compares the real cost of sending money to India from three major NRI corridors: the USA, the UK, and Germany. It breaks down bank wire fees, fintech platform costs, and exchange rate markups for each corridor using simple calculations on a standard transfer, then shows how PandaMoney delivers the real mid-market rate with zero fees across all three.

Most NRIs assume the cost of sending money to India is similar regardless of where they live. It is not. Fees, exchange rate markups, and available platforms differ meaningfully between the USA, the UK, and Germany. An India remittance fee comparison across these corridors reveals gaps that, over a year of regular transfers, add up to hundreds of dollars, pounds, or euros in unnecessary costs.

How to Read an India Remittance Fee Comparison Across Corridors

Before comparing corridors, it helps to understand what makes one transfer more expensive than another. The total cost of any Indian remittance has two parts, and most senders only notice one.

The Two Hidden Costs in Every India Remittance Fee Comparison

Cost 1: The transfer fee. This is the flat or percentage-based charge the platform displays upfront. It appears on your receipt. It is easy to spot and easy to compare.

Cost 2: The exchange rate markup. This is the cost most senders miss. Every platform converts your currency to INR at a rate slightly below the real mid-market rate and keeps the difference. Banks apply markups of 2% to 3.5%. Some fintech apps apply 0.5% to 1.5%. This never appears as a line item on your receipt. On a $1,000 transfer, a 2.5% markup costs you $25 silently.

Every comparison uses the full cost formula on a standard $1,000 / £1,000 / €1,000 transfer, making the numbers directly comparable across corridors.

India Remittance Fee Comparison: Sending from the USA

The USA is the single largest source of remittances to India. The corridor moves billions of dollars annually, yet most US-based NRIs still use their bank’s international wire transfer, which carries the highest combined costs of any sending method.

The current USD/INR rate sits near ₹95 per dollar, meaning every dollar lost to fees or markup equals ₹95 less for your family in India.

Best and Worst Options in the USA-India Remittance Fee Comparison

On a $1,000 transfer from the USA to India:

- US bank wire: $40 flat fee + 2.5% markup ($25) = $65 total cost. Your family receives ₹90,175 instead of ₹95,000 at mid-market

- Wise: ~$7 fee + no markup = $7 total cost. Your family receives ₹94,335

- Remitly: $0 fee (over $1,000) + 1% markup ($10) = $10 total cost. Your family receives ₹94,050

- PandaMoney: $0 fee + 0% markup = $0 total cost. Your family receives the full ₹95,000

The $65 cost of a US bank wire versus $0 with PandaMoney means a difference of ₹6,175 on a single $1,000 transfer. NRIs sending $2,000 monthly lose approximately $1,560 per year to avoidable bank costs.

US-based NRIs should also note that transfers above certain thresholds trigger IRS reporting requirements. The guide on transfer limits and IRS documentation requirements for large India transfers covers these compliance steps clearly.

India Remittance Fee Comparison: Sending from the UK

The UK is the second-largest NRI corridor to India. The pound currently trades near ₹128 to ₹129 per GBP, historically strong levels that make every pound of markup loss especially costly in rupee terms.

UK banks charge lower wire fees than US banks, but their exchange rate markups are comparable. The net result for UK-based NRIs is still a significant cost gap between bank wires and modern alternatives.

Best and Worst Options in the UK India Remittance Fee Comparison

On a £1,000 transfer from the UK to India:

- UK bank wire: £20 flat fee + 2.5% markup (£25) = £45 total cost. Your family receives ₹1,22,175 instead of ₹1,28,500 at mid-market

- Wise: ~£6 fee + no markup = £6 total cost. Your family receives ₹1,27,730

- Remitly: £0 fee + 1% markup (£10) = £10 total cost. Your family receives ₹1,27,215

- PandaMoney: £0 fee + 0% markup = £0 total cost. Your family receives the full ₹1,28,500

The £45 cost of a UK bank wire translates to ₹5,775 less rupees per £1,000 transfer. UK NRIs sending £1,500 monthly lose approximately £810 per year in combined fees and markup.

The pound’s current strength makes the UK corridor particularly attractive for sending money right now. For context on where GBP/INR is heading through Q3 2026, the GBP to INR forecast guide covers the key drivers and analyst projections.

India Remittance Fee Comparison: Sending from Germany

Germany has one of the fastest-growing Indian diaspora communities in Europe, driven by the IT and automotive sectors. German banks, including Deutsche Bank, Commerzbank, and the regional Sparkasse network, operate efficiently within the SEPA zone. However, SEPA does not apply to India, so every EUR to INR transfer goes through international wire infrastructure with its own cost structure.

The current EUR/INR rate sits near ₹110 to ₹111 per euro.

Best and Worst Options in the Germany-India Remittance Fee Comparison

On a €1,000 transfer from Germany to India:

- German bank wire: €20 flat fee + 2.5% markup (€25) = €45 total cost. Your family receives ₹1,05,325 instead of ₹1,10,500 at mid-market

- Wise: ~€5 fee + no markup = €5 total cost. Your family receives ₹1,09,945

- Remitly: €0 fee + 1% markup (€10) = €10 total cost. Your family receives ₹1,09,395

- PandaMoney: €0 fee + 0% markup = €0 total cost. Your family receives the full ₹1,10,500

The €45 cost of a German bank wire represents ₹4,950 less rupees per €1,000 transfer. German NRIs sending €1,500 monthly lose approximately €810 per year in avoidable costs.

For context on where the euro is heading against the rupee through Q3 2026, the EUR to INR forecast guide covers the ECB policy dynamics and key analyst projections.

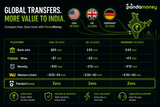

Full India Remittance Fee Comparison: USA vs UK vs Germany

Here is the complete side-by-side India remittance fee comparison across all three corridors on a standard transfer of $1,000 / £1,000 / €1,000.

Three things stand out from this India remittance fee comparison:

- Bank wires cost the most in every corridor, with the US corridor most expensive in absolute terms

- Wise and Remitly are genuinely better than banks, but still carry costs through fees or exchange rate markup

- PandaMoney delivers zero cost across all three corridors with same-day or next-day delivery

How PandaMoney Wins the India Remittance Fee Comparison Across All Three Corridors

The reason PandaMoney delivers zero cost in every corridor comes down to infrastructure. Traditional platforms route transfers through SWIFT’s correspondent banking network, which charges at each hop and applies exchange rate spreads to cover settlement risk.

PandaMoney routes through stablecoin rails (USDC/USDT) instead, settling on the blockchain in minutes and converting to INR through its network of 16+ fully authorised banking partners in India.

The annual savings for a regular NRI sender:

- US-based NRI sending $2,000/month via bank wire: saves approximately $1,560/year with PandaMoney

- UK-based NRI sending £1,500/month via bank wire: saves approximately £810/year with PandaMoney

- German NRI sending €1,500/month via bank wire: saves approximately €810/year with PandaMoney

Every transfer also creates a FEMA-compliant inward remittance record through PandaMoney’s authorised banking partners, giving your CA and Indian bank the documentation needed for tax filing, NRE account funding, and property transactions.

For a deeper look at how stablecoin infrastructure eliminates SWIFT costs entirely, the guide explains the mechanics behind the zero-cost model.

Download PandaMoney on Android or iOS.

FAQs: India Remittance Fee Comparison

Which Corridor Has the Highest Fees in the India Remittance Fee Comparison?

The USA corridor carries the highest absolute fees in this India remittance fee comparison. US banks charge $35 to $50 in wire fees, higher than typical UK (£15 to £25) or German (€15 to €25) bank charges. Combined with a 2% to 3.5% exchange rate markup, a $1,000 US bank wire typically costs around $65, compared to roughly £45 or €45 from the UK or Germany.

Does the Exchange Rate Affect the India Remittance Fee Comparison Between Corridors?

Yes, significantly. The UK corridor currently offers the most rupees per unit (approximately ₹128 to ₹129 per GBP), followed by the USA (approximately ₹95 per USD), then Germany (approximately ₹110 to ₹111 per EUR). A 2.5% markup costs more in rupee terms from the UK than from Germany, simply because each pound buys more rupees. The relative fee percentages are similar, but the absolute rupee impact differs by corridor.

Is Wise or Remitly Better for the USA to India India Remittance Fee Comparison?

On a $1,000 transfer, Wise costs approximately $7 (fee only, no markup) and Remitly costs approximately $10 (no fee over $1,000, but 1% markup). Wise wins slightly on cost for larger transfers because its fee is fixed rather than percentage-based. For smaller amounts, Remitly’s zero fee can be cheaper if the markup is low. Neither comes close to PandaMoney’s zero-cost structure.

Are the Fees the Same for All Transfer Amounts in This India Remittance Fee Comparison?

No. The exchange rate markup is percentage-based, so it scales with the transfer amount. A 2.5% markup on $5,000 costs $125, while the same markup on $1,000 costs $25. Transfer fees are often flat (a fixed dollar amount regardless of transfer size), which means the percentage impact of the fee decreases as you send more. For large transfers, the exchange rate markup dominates total cost by far.

How Does PandaMoney Deliver Zero Fees Across All Three Corridors?

PandaMoney bypasses the SWIFT correspondent banking network by routing transfers through stablecoin rails (USDC/USDT). The blockchain settles the transfer in minutes, removing the correspondent bank fees that traditional platforms pass on. The conversion to INR happens through PandaMoney’s authorised Indian banking partners at the real mid-market rate, with no markup added. The entire cost savings from removing the correspondent chain flows to the sender.

Disclaimer: This blog is for educational and informational purposes only. Fee estimates are based on publicly available data and typical market conditions as of May 2026. Actual fees and exchange rates vary by platform, transfer amount, payment method, and market conditions. Always verify live rates directly with your chosen platform before sending. PandaMoney facilitates all transfers exclusively through authorised and fully licensed banking and financial institution partners, ensuring full compliance with applicable RBI and FEMA guidelines. Verify current RBI inward remittance guidelines at rbi.org.in.

Related Articles

GetPandaMoney Inc. is a financial technology company, not a bank. Our product and services are offered in partnership with regulated and licensed financial institutions in each jurisdiction that we operate in. Client(s) deal directly with our regulated partners through the platform provided by PandaMoney.

For any queries or grievances, please write to us at compliance@getpanda.money

131 Continental Dr Suite 305 Newark, DE, 19713 US

©2025 PandaMoney. All Rights Reserved.

GetPandaMoney Inc. is a financial technology company, not a bank. Our product and services are offered in partnership with regulated and licensed financial institutions in each jurisdiction that we operate in. Client(s) deal directly with our regulated partners through the platform provided by PandaMoney.

For any queries or grievances, please write to us at compliance@getpanda.money

131 Continental Dr Suite 305 Newark, DE, 19713 US

©2025 PandaMoney. All Rights Reserved.