Cash Pickup vs Bank Deposit for India Remittances in 2026

This guide breaks down cash pickup vs bank deposit for India remittances in 2026. It explains how each method works under RBI rules, what the actual limits are, how the real costs compare once fees and exchange rate markups are stripped out, the compliance differences that matter for NRE deposits and future repatriation, and how to pick the right option based on who the recipient is and what the money is for.

India received $129.1 billion in remittances in 2024, the highest of any country in the world, making up 14.3% of all global remittance flows, according to the World Bank. Every one of those dollars, pounds, and euros eventually had to land somewhere. The two main landing spots are cash pickup at an agent location or bank deposit straight into the recipient’s account.

The two look similar on the surface. They feel completely different in practice. One gives your family cash in hand within minutes. The other leaves a full paper trail and unlocks options like NRE deposits, property purchases, and future repatriation.

This guide breaks down cash pickup vs bank deposit for India remittances with the real rules, numbers, and real trade-offs that matter in 2026.

What Cash Pickup vs Bank Deposit for India Remittances Actually Means

Both options are inward remittances regulated by the Reserve Bank of India under the Foreign Exchange Management Act (FEMA). The difference is the channel and the final delivery format.

Cash pickup routes through the Money Transfer Service Scheme (MTSS). You send money via an Overseas Principal like Western Union, MoneyGram, or Ria. The funds reach an Indian agent partnered with a bank or a Full-Fledged Money Changer (FFMC). Your recipient walks in with a photo ID and a reference number, and walks out with rupees in hand.

Bank deposit routes through either the Rupee Drawing Arrangement (RDA) or a regulated fintech remittance platform partnered with an Authorised Dealer (AD) bank in India. The money lands directly in your recipient’s savings, NRO, or NRE account. From there, they spend through UPI, debit card, or net banking.

The choice between the two is not about which is better in general. It is about which is better for your specific situation.

How Cash Pickup for India Remittances Works Under RBI Rules

Cash pickup is the older and simpler model. The recipient does not need a bank account, and the money is usually ready within minutes.

Cash Pickup Limits and Rules for India Remittances

The RBI sets clear limits on cash pickup under MTSS:

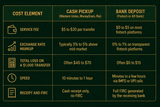

- Maximum per transaction: USD 2,500 (approximately ₹2.08 lakh)

- Maximum per recipient per year: 30 transactions, which works out to roughly ₹62.5 lakh annually

- Cash payout cap: ₹50,000 per transaction in cash. Amounts above ₹50,000 must be paid by account-payee cheque, demand draft, or bank credit, not in cash.

- Allowed purposes only: Personal family maintenance and help to foreign tourists in India

- Not allowed: Business payments, charitable donations, NRE deposits, property purchases, or investments

The recipient needs a valid photo ID (Aadhaar, passport, voter ID, or driving licence), and the name on the ID must match the name the sender used.

When Cash Pickup for India Remittances Makes Sense

Cash pickup still has a clear role in 2026, even with India’s strong banking and UPI infrastructure. It works well when:

- The recipient does not have a bank account, which is still the case in some pockets of rural and semi-urban India

- You need to send emergency funds within minutes, and the recipient cannot wait for a transfer to clear

- The recipient is travelling within India and needs cash on hand

- The amount is small and one-off, like ₹10,000 or ₹20,000 to a relative

Speed is the real strength here. A Western Union or MoneyGram cash pickup can be ready in as little as 10 to 15 minutes once the sender confirms the transfer.

How Bank Deposit for India Remittances Works in 2026

Bank deposit is now the default for most NRI senders. With over 53 crore Jan-Dhan accounts opened in India and UPI processing more than 15 billion transactions a month, almost every Indian household has a bank account that can receive money instantly.

Bank Deposit Limits and Channels for India Remittances

Bank deposits under the Rupee Drawing Arrangement (RDA) are far more flexible:

- No upper limit on personal remittances like family maintenance, gifts, education, or medical expenses

- Cap of ₹15 lakh per transaction for trade-related inward remittances

- Funds can land in savings, NRO, NRE, or FCNR accounts, depending on the purpose

- Delivery rails include NEFT, RTGS, IMPS, and direct credit, often within minutes

- FIRC (Foreign Inward Remittance Certificate) is generated automatically by the receiving bank, which serves as legal proof of the transfer

For a deeper dive on why this document matters, see our guide on what FIRC is and why every NRI needs to request it.

When Bank Deposit for India Remittances Makes Sense

Bank deposit is the right choice in almost every situation that is not an emergency cash request. Specifically:

- Recurring family support of any amount, since there is no annual transaction cap

- Large one-time transfers above ₹50,000, where cash payout is not legally allowed anyway

- NRE or NRO deposits, since MTSS cannot route money into these accounts

- Property purchases, investments, or business funding in India all of which require a proper paper trail

- Cases where you want a clean FIRC for future repatriation or tax filing

If the recipient has any bank account, bank deposits win on cost, safety, and flexibility almost every time.

Cash Pickup vs Bank Deposit for India Remittances: Cost Comparison

This is where the two options really separate. The headline fee is rarely the full cost. Most of the difference hides in the exchange rate markup.

On a single $1,000 transfer, the difference can look small. Over a year of sending $1,000 a month, the gap is often $500 to $700 saved by choosing a bank deposit on a transparent platform. For a full comparison across providers and channels, our guide on Western Union vs bank wires vs fintech apps for India remittances covers every option.

Compliance Difference Between Cash Pickup and Bank Deposit for India Remittances

The compliance gap is even bigger than the cost gap.

Cash pickup under MTSS is strictly personal use only. It cannot be used for business income, charitable donations, NRE deposits, property purchases, or any investment activity. It also does not generate an FIRC, which means there is no formal proof that the money entered India through proper channels.

Bank deposit under RDA generates a full FIRC, supports every legitimate purpose code, and creates the paper trail you may need later for:

- Future repatriation of funds back abroad. Our guide on NRO account repatriation and the USD 1 million annual limit explains why this paper trail matters

- NRE account credits, which are tax-free and freely repatriable, and which cannot accept MTSS funds at all

- Property purchases in India, where the source of funds must be traced cleanly

- Tax filing in India, the US, or the UK, if questions come up about the source of money

Cash pickup is fine for everyday family support. A bank deposit is the only safe choice if the money has any future financial purpose.

How to Choose Between Cash Pickup and Bank Deposit for India Remittances

Pick cash pickup if:

- The recipient has no bank account

- You are sending under ₹50,000 as one-off support

- The need is urgent, and the recipient cannot wait

- You do not need any documentation for the transfer

Pick bank deposit if:

- The recipient has an active Indian bank account

- The amount is above ₹50,000

- The money is for NRE deposits, property, or investments

- You want the lowest possible cost

- You may need an FIRC later for tax or repatriation purposes

Also, be aware of safety. Carrying large cash amounts home from a pickup location is a real risk, and scammers frequently target newly arrived cash recipients.

Our guide on the red flags that expose remittance scams targeting NRIs covers the warning signs to watch for.

How PandaMoney Handles Cash Pickup vs Bank Deposit for India Remittances

PandaMoney is built for fast, transparent, bank-deposit-first remittances to India. Every transfer routes through its network of 16+ fully authorised banking and financial institution partners in India, with the money landing directly in the recipient’s savings, NRO, or NRE account.

The platform is designed so legitimate users get the full benefits of a bank deposit without the friction:

- Real Google mid-market exchange rates, so 100% of your intended amount reaches India

- Zero hidden fees on supported corridors, with no exchange rate markup that eats into the recipient’s amount

- Direct deposit to any Indian bank account via IMPS and NEFT, often settled within minutes

- Clean paper trail for FEMA compliance, including the FIRC generated by the receiving bank

- No crypto wallets, no blockchain knowledge required. PandaMoney uses stablecoin settlement rails purely in the backend for speed and lower cost.

To understand the infrastructure clearly, see our explainer on how stablecoin rails work for international money transfers.

If your recipient is on a joint NRE account, our guide on holding a joint NRE account with a resident Indian covers what the RBI allows.

Download PandaMoney on Android or iOS and send your next bank deposit transfer with full transparency.

FAQs: Cash Pickup vs Bank Deposit for India Remittances

Is Cash Pickup Still Worth Using for India Remittances in 2026?

Yes, but only in specific cases. Cash pickup makes sense when the recipient has no bank account, when you need to send a small amount within minutes, or in genuine emergencies. For everything else, a bank deposit is cheaper, safer, and gives you a full paper trail through the FIRC issued by the receiving bank.

Can I Send Money to an NRE Account Through Cash Pickup?

No. The Money Transfer Service Scheme that governs cash pickup is strictly for personal family maintenance and to help foreign tourists. NRE deposits are not allowed under MTSS. You must use the Rupee Drawing Arrangement through a bank or a regulated fintech platform to credit an NRE account legally.

Is Bank Deposit Cheaper Than Cash Pickup for India Remittances?

Yes, in almost every case. Cash pickup providers like Western Union and MoneyGram typically apply a 3% to 5% exchange rate markup plus a service fee, costing $40 to $70 on a $1,000 transfer. Transparent bank deposit platforms charge close to mid-market rates with very low or zero fees.

What Is the Maximum Cash Pickup Amount Allowed in India?

No single transaction can exceed USD 2,500 under MTSS, and cash payout in hand is capped at ₹50,000 per transaction. Anything above ₹50,000 must be paid by account-payee cheque, demand draft, or direct bank credit. The recipient is also limited to 30 MTSS transactions per calendar year.

Do I Get an FIRC for a Cash Pickup Transfer to India?

No. Cash pickup under MTSS does not generate a Foreign Inward Remittance Certificate. The recipient gets a cash receipt only. If you need an FIRC for tax filing, NRE deposits, property purchases, or future repatriation, you must use a bank deposit through an Authorised Dealer bank or a regulated fintech platform.

Disclaimer: This blog is for educational and informational purposes only. It does not constitute legal, tax, or financial advice. Inward remittance rules to India are governed by the Reserve Bank of India under the Foreign Exchange Management Act, 1999, including the Money Transfer Service Scheme (MTSS) and the Rupee Drawing Arrangement (RDA). Limits, exchange rates, fees, and scheme details may change over time, and individual circumstances vary. Senders should consult their remittance provider and, where relevant, a qualified chartered accountant or compliance professional.

Related Articles

GetPandaMoney Inc. is a financial technology company, not a bank. Our product and services are offered in partnership with regulated and licensed financial institutions in each jurisdiction that we operate in. Client(s) deal directly with our regulated partners through the platform provided by PandaMoney.

For any queries or grievances, please write to us at compliance@getpanda.money

131 Continental Dr Suite 305 Newark, DE, 19713 US

©2025 PandaMoney. All Rights Reserved.

GetPandaMoney Inc. is a financial technology company, not a bank. Our product and services are offered in partnership with regulated and licensed financial institutions in each jurisdiction that we operate in. Client(s) deal directly with our regulated partners through the platform provided by PandaMoney.

For any queries or grievances, please write to us at compliance@getpanda.money

131 Continental Dr Suite 305 Newark, DE, 19713 US

©2025 PandaMoney. All Rights Reserved.